I value Tesla at $300/share ($60 after the forward split on 8/28/20), let’s see why…

Is Tesla worth $2000/share? This is a million dollar question that is bothering everyone. 35 analyst firms that track Tesla are not able to make up their minds and their opinions are divided. In this blog, I will provide my reasons to why I am bearish on Tesla stock.

So what is Tesla? Tesla is world’s most valued automobile company, currently valued at around $381B. Tesla is also an automotive company that is defining the future of self driving and electric cars. I also count Tesla as one of the most sophisticated information technology companies. Tesla was founded in 2003 and in 2008 it launched Roadster which unveiled Tesla’s cutting edge battery technology and electric powertrain. Currently, Tesla has four models in the market (Model 3, Y, S, X) with a plan to launch Roadster 2, Cyber truck and Semi in the coming years. In addition to the car business, Tesla also generates its revenues from solar generation and storage products.

Revenue Projections

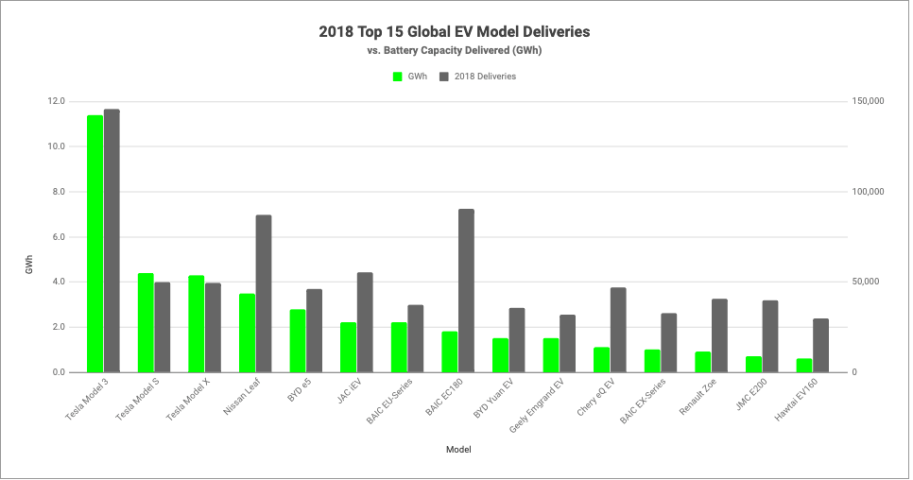

We can certainly argue that most of the companies in Table 1 have spent a lot more time in market than Tesla. We can also argue that Tesla is the best technology available in the market. I will agree with both comments but the fact is that Tesla does not have a profitable business. There is no doubt that deliveries for Tesla are increasing and that makes Tesla a clear winner in the PEV (Plug-in Electric Vehicle) and BEV (Battery Electric Vehicle) categories. Two tables below show the US (only) deliveries from 2009 to 2019 for PEV and BEV categories. The tables are sorted in descending order of total sales from 2009 to 2019. The data shows Tesla owns 53% of the US market share in the PEV and BEV categories. Globally it controls 16% of the market share.

I have used the data in tables above to develop trends for the EV market and also model Tesla’s dominant position. But let us start with evaluating the EV market and how it is projected to behave in the coming years. Based on various trends and analysts forecasts we know that electric vehicle market will continue to expand. Some of the factors that can contribute to its growth include favorable government policies and subsidies, heavy investments from automakers in EVs, growing concerns over environmental pollution, demand for increased vehicle range per charge and a major increase in availability of EV models. We have seen EV grow at a staggering pace of around 65% from 2017 to 2018. But in 2019, the number of units sold increased only by 9%, from 2.1 million to 2.3 million. Globally, EV represented 2.5% of total vehicle sales which is 5x more compared to 0.5% in 2015. Trends also indicated that key EV market is shifting regional dynamics, with China and the United States losing ground to Europe. EV sales remained constant in China in 2019, at around 1.2 million units sold (a 3 % increase from the previous year). In the United States, EV sales dropped by 12 percent in 2019, with only 320,000 units sold. Meanwhile, sales in Europe rose by 44 percent, to reach 590,000 units. These trends continued in first-quarter of 2020 as EV sales decreased from the previous quarter by 57 percent in China and by 33 percent in the United States. In contrast, Europe’s EV market increased by 25 percent.

Market research companies continue to demonstrate strong demand for EVs in the coming years. Current trends and COVID are creating a lot of uncertainties in the supply chain and logistics. Based on market research report from market and market, the EV industry is poised to grow at 21% CAGR. Tesla had a Global market share of 16% in 2019 (Model 3 itself contributed 13%), which is down from 18% in 2018 in the EV space. Though various studies point at different growth figures, I am assuming that EV industry will deliver ~27M units by 2030 and that Tesla’s market share will reduce to 10% by 2030. The reason to reduce Tesla’s share to 10% is based on the declining trend in Tesla’s global market share and sheer competition from BYD (China), BMW (Germany), Nissan (Japan) and Volkswagen (Germany). Furthermore, there are 24 other companies ready to leave the mark in this crowded market.

Based on information present in Tesla’s 10Q form for 2020 and 10k from 2019 Tesla’s Gross profit is around 13% for Model 3/Y and 19% for Model S/X. For Roadster 2, I am assuming a gross profit of around 40% based on similar industry category cars from Jaguar, Porsche and Ferrari. For Tesla pick up truck, I am assuming a gross profit of around 12.5% based on similar models by GM, Ford and Fiat. For Tesla Semi, I am assuming a GP of 19% based on similar observations from Paccar, MAN and Scania.

Energy generation, storage and services: Tesla does not disclose its earning in MWs of generation or storage. It is difficult to put right guestimate of Tesla’s share in this segment. However, it faces stiff competition from big players like Lockheed Martin, AES and Siemens. In lieu of evidence, I am assuming the total revenue from this section will grow at around 10% CAGR. This 10% is based on the fact that Tesla will retain its current market share and support the 10% CAGR in storage and generation market space based on various analyst predictions.

Economic Moat

Automotive Market: According to me, Tesla is still very young. Governments are framing regulations that could change the course of how this market will be defined. Further, Tesla will most likely remain the car for the rich. With advancement in technology the company is looking to reduce the cost of production. But let us consider facts – its cheapest car is around $42,000. Elon Musk in an interview in 2014 stated “I think we will (produce cheap car), but this is not a bold assertion we unequivocally will. There is a possibility we may not.”

Tesla’s growth runway looks lucrative, but this growth also requires constant substantial reinvestment in platforms. The eventual output limit of Fremont factory is uncertain, as is the cadence of Tesla opening new plants overseas. During this growth phase, there will almost certainly be a recession or two. In times of economic uncertainty, it is difficult to say what Tesla’s sales volume will be or what access, if any, the firm will have to capital markets. Tesla wants between 10 and 12 Gigafactories in the long term to manufacture the projected 2.5M EVs, currently it only has 3 active and one under construction.

Tesla’s long range batteries gives it a huge advantage over pure EVs on the market (402-mile EPA range for the long-range Model S versus about 300 for the Ford Mustang Mach-E, 259 miles for the Chevrolet Bolt, 226 miles for the Nissan Leaf, 234 miles for the Jaguar I-PACE, and 204 miles for the Audi e-tron). Below is a chart showcasing sales of total Toyota Prius and Telsa’s over the last 15 years in US

For evaluations purposes I am considering Tesla’s competition to be the entire auto industry rather than just EVs market. Musk’s own words do not support efficient scale. He wrote in a June 12, 2014, blog post announcing that Tesla would not sue companies that use its patented technology in good faith: “Given that annual new-vehicle production is approaching 100 million per year and the global fleet is approximately 2 billion cars, it is impossible for Tesla to build electric cars fast enough to address the carbon crisis. By the same token, it means the market is enormous. Our true competition is not the small trickle of non-Tesla electric cars being produced, but rather the enormous flood of gasoline cars pouring out of the world’s factories every day.” As we can see from charts below the production capacity has increased substantially to around ~350k units/year in the last two years but Tesla still needs to grow production by 6x to meet the projected deliveries of ~2.3M units by 2030.

Energy generation, storage and services: Could not access. Considering that market is very crowded, there is no moat in this segment.

Fair Value Evaluation

Let me start this section by stating that there is no alternative in current market for Tesla’s autonomous vehicles. Tesla’s technology is unmatchable and unbeatable even by its closest peers. Based on the growth model evaluated earlier I am projecting that Tesla will delivery around ~13M units in the next 10 year. Further, I am using the operating expenditure at 12% (based on industrial average of similar automakers). These parameters result in Weighted average cost of capital (WACC) of 12.7%. Which results in a fair price of $300.7

We must remember, this share price is based on industry projections of ~27M units of EV’s by 2030. If this number shrinks, an equivalent reduction in revenue will occur of Tesla further reducing the fair value. Just to ensure I am capturing the worst, base and best case scenarios I developed the model for both optimistic and pessimistic situations. My fair value ranges from $50 to $300 ($15 to $60 after forward split on 8/28/20). Tesla according to my DCF model and industry prediction is around 600% overvalued. I will not pay more than $300 at this time for a Tesla share.

Disclosure: I do not own any stocks in TSLA. I do not intend to take a short or a long position in any of the stocks or organizations mentioned in this blog in the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

References

https://www.iea.org/reports/global-ev-outlook-2020

https://about.bnef.com/electric-vehicle-outlook/

https://www.iea.org/reports/global-ev-outlook-2020

Leave a Reply