Fears of inflation, recession, and slow growth are top of the worries interrupting the sleep of many CEOs around the world. Survey stated, 93% of CEOs are preparing for a US recession over the next year or so. Close to 51% of CEOs say that they aren’t expecting the economy to pick up steam until late 2023 or even 2024.

Overall, looking at the data available and ongoing speculation of an upcoming recession leaves things somewhat open-ended at this moment. Consumer demand, while not where it previously was, is still decent. This keeps the outlook for 2023 pretty open. Several open topics include Russia’s war on Ukraine and the West’s dependence on imports from China. On top of this continuous emphasis on environmental challenges to reduce CO2 is keeping companies on building environmentally friendly practices which are cost now at the expense of predicted future returns.

Before we jump into banks that are creating a recessionary environment, I want to quickly make sure the readers understand the concept of recession and the factors that cause a recession. We have all been talking about recession but an understanding of the term is really important to access the future outlook.

Investopedia is a great source to understand the simple investment and financial concepts and I have lifted this definition from their page.

A recession is a significant, widespread, and prolonged downturn in economic activity. A common rule of thumb is that two consecutive quarters of negative gross domestic product (GDP) growth mean recession, although more complex formulas are also used.IMF has reduced baseline forecast for growth from 3.4% in 2022 to 2.8% in 2023 and this figure

Economists at the National Bureau of Economic Research (NBER) measure recessions by looking at nonfarm payrolls, industrial production, and retail sales, among other indicators, going far beyond the simpler (although not as accurate) two quarters of negative GDP measure.Let us break down this newsletter’s primary components and what we will be talking about.

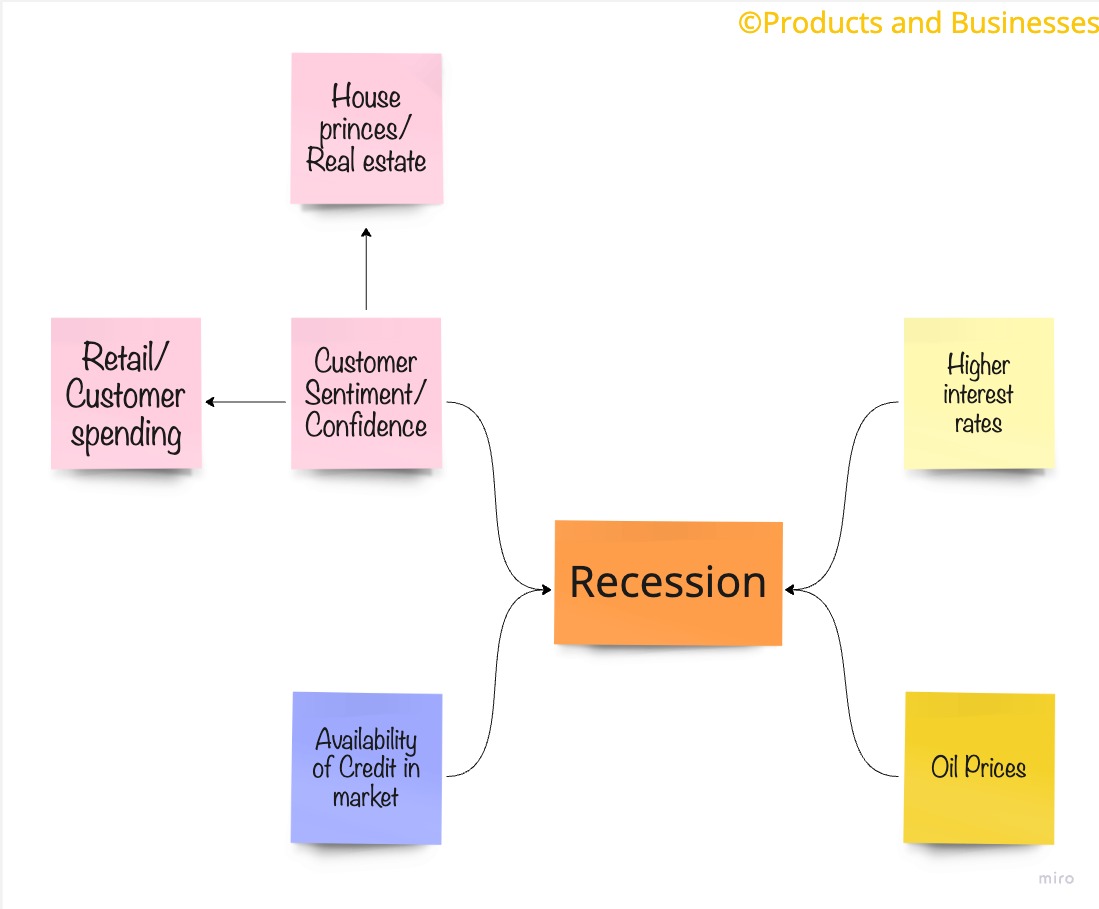

However, there are no fixed rules about what measures or contributes to a recession. I am currently looking at the factors in the image below to create a forecast for the markets.

In the previous newsletters, I have covered Sentiments and Retail spending. I also explained the pandemic phenomenon explaining supply and demand. You can read it here.

In today’s newsletter, I want to focus on interest rates and the credit crunch in the markets. I will be using banks as an example and understand the impacts of a “run on the bank”. Lastly, where do we stand with the recession?

Table of Contents

Health of banks

Financial institutions always look forward to a higher interest environment whereas during the pandemic the swift pace of Fed rate hikes has sparked higher recessionary fears. It is forcing investors, startups, and organizations to spend capital with a focused and disciplined approach.

Silicon Valley Bank (SVB) on March 10, 2023, became the second largest bank failure in US history surpassing the bank failures of the 2008 financial crisis. During the period of near-zero interest during the pandemic, SVB invested heavily in US government bonds. This strategy backfired as the fed’s started to raise interest aggressively to curb inflation. As interest rates climbed, bond prices fell, resulting in the decline of SVB’s bond portfolio and its ultimate collapse.

Let us understand what happened with SVB.

- SVB is based in Silicon Valley, California. Borrowers of SVB were mainly tech startups, so there’s a concentration of money in one sector. When inflation started rising and borrowing costs become high, many companies started to struggle to get additional financing from VCs. As a result, they needed cash to run operations and these companies went to the SVB to withdraw all their money. This is called “run on the bank”. SVB did not have all the money handed in as it has been invested. Here is the start of the second problem.

- SVB had invested $86B of the portfolio in long-duration securities, mostly agency-issued mortgage-backed securities. Per their 10-k the average yield of these securities was 1.63%. These securities were “held to maturity (HTM)”. The bonds would have been worth more if they were held to maturity. As the demand for cash increased (from point 1 above), SVB had to sell these bonds quickly and at a loss. As a result, SVB tried to raise money by issuing its own bonds on the open market. This created uncertainty among their customers. A perfect storm hit SVB.

How are big banks doing?

It’s great to be a mega bank in this crisis situation. Where some of the small and mid-sized banks are struggling for traction, JP Morgan Chase – the largest bank in the US is thriving in the world of rising interest rates. JP Morgan posted a 52% increase in first-quarter profits and record revenue. Citi and Wells Fargo also benefited from panicky depositors who are flocking away from small and mid-sized banks to large banks for their deposits. JP Morgan estimated it had picked up about $50B in new deposits following the March bank failures.

Big banks are facing headwinds as well. From WSJ:

Despite the windfall from some smaller-bank customers, deposits are becoming less plentiful and more expensive. The stress at banks has prompted some customers to move their money to Treasurys and money-market funds.Delinquencies.

Between the end of December and the end of March, deposits rose at JPMorgan, but fell at Citigroup and Wells Fargo as businesses and wealthy customers moved their money in search of higher rates

In the current situation, banks are being pressured to pay high rates on deposits.

The average yield for online savings accounts rose to about 3.75% in March, according to indexes from Deposits Online LLC, compared with 0.5% a year ago. Online one-year certificates of deposits on average offered an annual percentage yield of nearly 4.75%, up from less than 1% in 2022.

Even America’s biggest banks are paying more to keep customers from taking their business elsewhere. Citigroup Inc. paid 2.72% on interest-bearing deposits in the first quarter, up from 2.1% at the end of 2022. JPMorgan Chase & Co. paid 1.85%, up from 1.37%, while Wells Fargo & Co. paid 1.22%, up from 0.70%.

Delinquency – Not a problem at the current moment

The US mortgage delinquency and foreclosure rates remained consistently low through 2022 and closed at around 3%. Here is the corelogic chart, Corelogic calculates delinquencies across the country.

Delinquencies and defaults on household debts typically closely follow the business cycle. As economic conditions deteriorate, falling employment and reduced incoming puts a strain on family finances leading to missed debt payments and defaults. Lower delinquency report indicates households are still comfortable paying off debts.

One reason for low delinquencies is low-interest rates on covid time loans. It’s important to follow this data going late into 2023 as the families that made home or car purchases in late 2022 or early 2023 got high-interest rates which could be a troubling sign for a sharp increase in mortgage delinquencies.

In the short term, falling home prices are likely to push the mortgage delinquency rate up. Many homeowners who bought homes in the last 24 months have little to no equity. Selling homes at steep discounts during the pandemic high will hurt buyers and increase delinquencies in the future.

After looking at the latest data on inflation, home prices, personal savings, and household incomes it seems to me that mortgage delinquency rates will increase in 2023 and will continue to rise in 2024.

Conclusion

I believe the immediate impact of SVB’s failure is two-fold. Firstly, the implication on its client base or customers and secondly on the health of the banking system in general. Impact on the customer base is being handled by Feds via FDIC and creating liquidity for the banks that are facing the financial crunch. However, the second part which is the impact on the banking system is still unfolding. Looking forward, I believe there will be heavy scrutiny of mid and small-sized banks and more proactive regulatory involvement. There could be a possible scenario in that deposits are moved from these banks to large banks.

Impacts of tight scrutiny on banks will create credit unavailability in the market as banks will try to tighten lending which will create a slowdown in the economy. If you are an investor, it means your cyclical stocks will be negatively impacted and growth stocks will be rewarded. This is bad news for small companies as getting cash will become challenging however big companies with a track record of paying back debt will be rewarded in case they require cash. This should slow down the number of IPO launches in the next two years.

Cheers

Leave a Reply